.jpeg)

TL;DR:

In mortgage, the first lender to reach a rate-shopping borrower usually controls the deal, and "first" means minutes, not hours. An MIT/InsideSales analysis found the odds of qualifying a lead fall about 21x when callback time slips from 5 minutes to 30. Yet in a study of 114 B2B companies, more than 99% never responded within 5 minutes. The fix isn't one tool; it's three channels firing at once: an instant text, a sub-60-second callback, and a safety net for missed calls.

Key facts:

- Qualification odds drop roughly 21x when mortgage callback time goes from 5 to 30 minutes (MIT/InsideSales).

- Qualification chances fall about 4x between minute 5 and minute 10. The window is that tight.

- More than 99% of companies don't respond within 5 minutes; of those that call, only 42% manage it within the hour.

- Rate-shoppers fill out 3 to 4 lender forms in one sitting. Speed, not pitch, decides who they talk to first.

- Aloware runs Form2Text, Form2Call, and AI Call Rescue in parallel, and logs every touch to your CRM automatically.

A lending team I worked with last year told me their loan officers "always responded same day." They were proud of it. Then we looked at where their purchased leads were actually going: a borrower submitted a form at 9:14 a.m., it landed in a shared queue, and an LO picked it up after lunch. By then the borrower had already talked to two other lenders and half-committed to one. The team wasn't lazy. Every person on it was working hard. They were just losing to the clock, and they couldn't see it because "same day" felt fast.

That gap between "we follow up fast" and actually-fast is where mortgage pipelines quietly leak. If you're buying leads and your response time is measured in hours, you're paying full price for borrowers your competitors are closing. Here's the operational playbook to fix it.

Why mortgage teams lose deals in the first five minutes

Mortgage is one of the most response-sensitive verticals there is, for one structural reason: the borrower is shopping more than one lender at the same time. A rate-shopper rarely fills out a single form. They fill out three or four, a marketplace, two direct lenders, maybe their own bank, inside the same browsing session. Every one of those lenders gets the same lead at roughly the same minute.

So the competition isn't really about who has the best rate sheet. At the moment of contact, the borrower hasn't compared rates yet. They're comparing who picked up. The lender who reaches them first gets to frame the conversation, set expectations, and start the application while everyone else is still sitting in a queue. The first real human voice usually wins the relationship, and the loan tends to follow the relationship.

This is why an AI text agent that replies the second a form lands matters more in mortgage than in almost any other category. The acknowledgment alone buys you a place in line while a loan officer dials.

Key takeaway: In mortgage, you're not competing on rate at the moment of contact. You're competing on who reaches the borrower first. Speed is the product.

What is a good mortgage lead response time?

A good mortgage lead response time is under five minutes from form submission to first live contact, and the closer you get to one minute, the better your odds. The widely cited Lead Response Management study (run with MIT's Professor Oldroyd using InsideSales.com data across more than 100,000 call attempts at six companies) found a roughly 100-fold increase in the odds of reaching a lead and a 21-fold increase in the odds of qualifying one when response time was held to 5 minutes instead of 30. The decay inside that window is steep, too: qualification chances dropped about fourfold between minute 5 and minute 10.

Translate that to a mortgage desk. A 30-minute callback isn't "a little slower" than a 5-minute one. On the qualification math, it's a different business. And five minutes is not a stretch goal; it's the threshold where the curve is still in your favor. Under 60 seconds, across more than one channel, is where the best mortgage teams now operate.

Key takeaway: Treat 5 minutes as the outer edge of acceptable and under 60 seconds as the target. The qualification curve falls off a cliff after the first few minutes.

Why "we follow up fast" usually isn't fast

Most mortgage teams genuinely believe they respond quickly. The data says otherwise, and not because anyone is slacking. In a study of 114 B2B companies, more than 99% failed to respond within five minutes. Only 31% ever called the lead by phone at all, and of those, just 42% managed it within the hour. The average time to a phone response was more than 14 hours.

Here's the operational diagnosis. "Fast" breaks down at the handoff, not the intent:

- The queue problem. Leads land in a shared list or round-robin and wait for whichever LO is free. "Assigned in minutes" is not "contacted in minutes."

- The single-channel problem. A lot of teams "respond" with an automated email the borrower never opens, then count it as a touch. Email is not contact.

- The after-hours problem. Mortgage leads come in at 9 p.m. and on weekends. If your response depends on a human being at a desk, your real response time is "next business morning."

- The context problem. When an LO finally calls, they're cold, no idea what the borrower asked for, so the first call is slow and clumsy even when it's quick.

Every one of these is a systems gap, not an effort gap. You can't fix a systems gap by telling people to try harder. You fix it by making the first response happen without waiting on a human.

Key takeaway: "Assigned fast" and "emailed fast" feel like speed but don't count as contact. Real response time is measured to the first live human touch, and that's where queues quietly cost you loans.

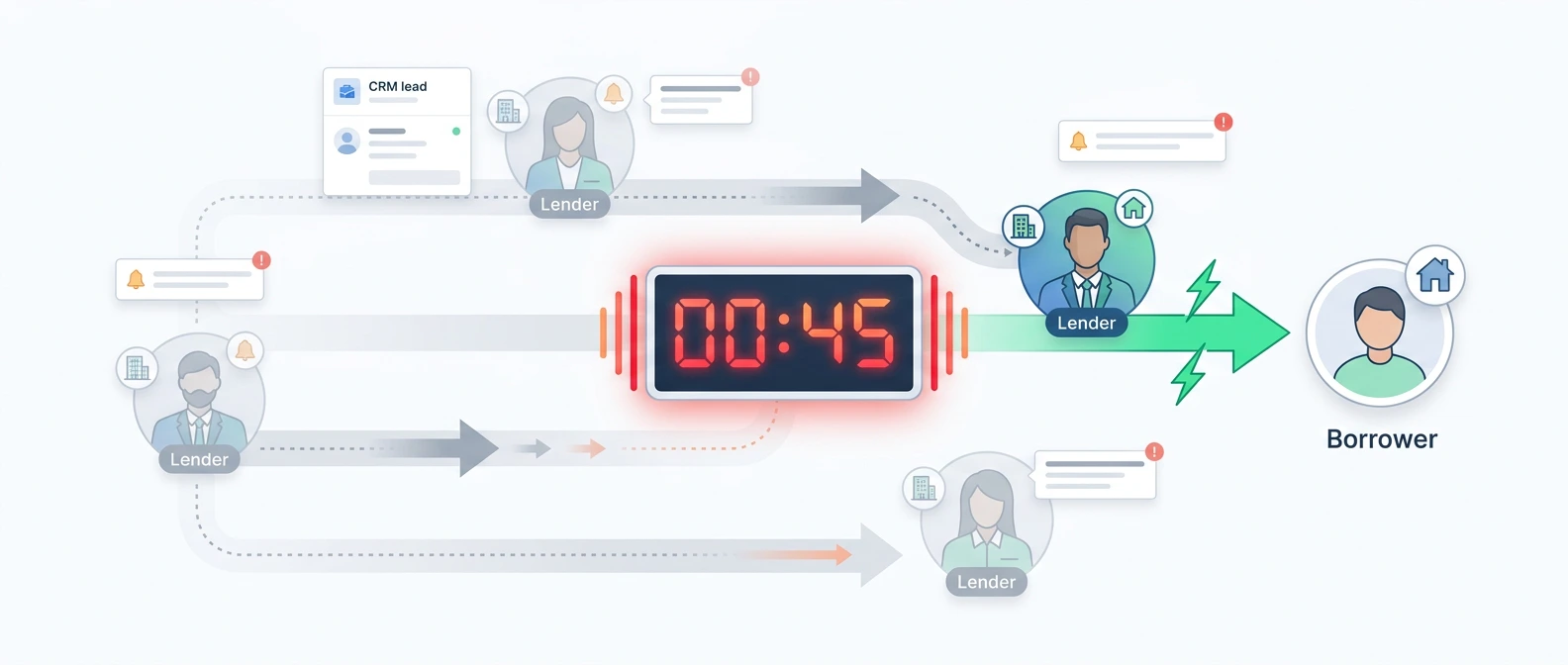

The 60-second mortgage response playbook

Here's the playbook I give mortgage teams that want to stop losing rate-shoppers. The principle: the moment a form submits, more than one thing should happen at once, and none of it should wait on a person being free.

- Fire an instant text (0 to 10 seconds). A personalized SMS to the borrower the second the form lands: name, what they asked about, and a one-line "a loan officer is calling you now." This buys your place in line even if every LO is on a call.

- Trigger a sub-60-second callback (under 1 minute). The lead routes straight to an available loan officer's phone with the borrower's details on screen, so the first call is warm and informed, not a cold "uh, who is this?"

- Catch the misses automatically. When no LO can pick up, after hours, lunch rush, everyone dialing, a missed-call handler answers so the borrower never hits dead air, captures intent, and logs it for first-thing follow-up.

- Log everything to the CRM as it happens. Every text, call, and recovered miss writes back to the borrower's record automatically, so the next LO touch has full context and nothing falls through.

Notice none of these steps is a person remembering to do something fast. That's the whole point. And because the borrower's callback is an outbound call, your callback still has to actually get picked up. Speed only pays off if the call connects.

Key takeaway: Speed-to-lead in mortgage means text, call, and missed-call recovery firing in parallel the instant a form submits, with zero dependence on a human being free.

How does Aloware hit sub-60-second response across channels?

This is the part most "speed-to-lead" tools get wrong: they own one channel and call the job done. Aloware runs the whole playbook above as one connected system inside your CRM.

- Form2Text sends a personalized SMS the moment a form is submitted, pulling the borrower's name and request straight from the form fields. It works with native HubSpot forms and, through webhooks and Zapier, with marketplace and ad-platform leads too.

- Form2Call rings a loan officer within about 60 seconds of the submission, with the lead's context previewed before they connect. After-hours leads queue to the top of the next morning's call list, so nothing rots overnight.

- AI Call Rescue is an account-level missed-call handler: when an inbound call goes unanswered, a system-managed AloAi voice agent answers it, greets the caller, captures intent and contact details, records and transcribes the conversation, and can kick off a follow-up workflow. The call stops being a "missed call" and becomes a logged lead. (AloAi voice is billed per AI talk-minute, from $0.10/min; it's an add-on, not bundled into a seat.)

- Native CRM logging ties it together. Every one of those touches writes to the borrower's contact record automatically, so your LOs proactively work from a complete timeline instead of reconstructing it.

For teams that want the inbound side fully automated, Aloware's AI voice agent built for mortgage teams can qualify the borrower, collect documents over SMS, and book the loan-officer appointment, while staying clear of licensed activities like quoting rates.

If you're losing rate-shoppers to slow follow-up, this is worth seeing live. Book a 20-minute demo and we'll show Form2Call, Form2Text, and AI Call Rescue running in parallel on a sample mortgage lead.

Key takeaway: Aloware's edge isn't a faster autoresponder; it's text, call, and missed-call recovery working as one CRM-logged system, so "sub-60 seconds across channels" happens without anyone babysitting it.

What does a slow mortgage lead response actually cost?

Run the numbers on your own pipeline and the leak gets concrete fast. Say you buy 300 mortgage leads a month at $45 each, that's $13,500 in lead spend. Now say half of those, 150, are active rate-shoppers comparing lenders in the same session. On the lead-response data, the lender reaching them in 5 minutes qualifies them at many times the rate of the lender reaching them in 30. If a 30-minute average is handing the bulk of those 150 rate-shoppers to whoever called first, you're not losing a rounding error. You're funding your competitors' funnels with leads you paid for.

You don't need precise conversion figures to feel it. One extra qualified borrower a week from leads you already bought, at a typical mortgage commission, pays for the entire speed-to-lead setup many times over. The cost of staying slow isn't the software you didn't buy. It's the loans that closed somewhere else.

Key takeaway: The expensive line item isn't a speed-to-lead system. It's the rate-shoppers you already paid for and handed to a faster competitor.

Common implementation pitfalls for mortgage teams

Speed-to-lead is straightforward to stand up, but mortgage has a few vertical-specific traps. Watch these:

- Texting before you've squared away consent. A borrower who submits your form has typically given express consent to be contacted, which is what keeps the instant text and callback clean, but that depends on how your form and disclosures are configured. Set it up with proper consent language and registered A2P 10DLC senders, and don't improvise the legal side; loop in whoever owns compliance for your shop.

- Letting callback numbers burn. If you're dialing high volume off a handful of numbers, carriers start flagging them "spam likely," and a sub-60-second callback that shows up as spam is a wasted callback. Monitor reputation so it doesn't quietly decay; Aloware's number-reputation monitoring exists for exactly this.

- No plan for after-hours and weekends. A meaningful share of mortgage leads arrive when no LO is available. If your only fast channel is a live human, decide now what catches the 9 p.m. submission, a missed-call handler or an inbound AI voice agent, or you've just built a fast system that's only fast during office hours.

- Treating automation as a replacement for loan officers. It isn't. The instant text and the missed-call catch buy time and hold the borrower's attention; the LO still closes. Teams that frame it as "the robot does the selling" set the wrong expectation and under-staff the human side.

Key takeaway: The failure modes are operational, not technical: unmanaged consent, burned callback numbers, no after-hours plan, and over-trusting automation. Plan for all four before you flip it on.

The bottom line

Mortgage rewards speed more honestly than almost any vertical: the borrower is shopping several lenders at once, and the one who reaches them first usually keeps them. The teams losing those deals aren't slow because they're careless. They're slow because they're running a queue instead of a system. Replace the queue with three channels that fire the instant a form submits, log everything to the CRM, and make sure the callback actually connects, and "we respond fast" stops being a feeling and starts being a number you can defend.

If your mortgage team is buying leads and measuring response time in hours, that's the first place to look this quarter. Grab 20 minutes with us and we'll map your current form-to-first-contact flow and show you where the minutes are going. Bring a real lead source and we'll trace it end to end.

Frequently Asked Questions

What is a good lead response time for mortgage leads?

Under five minutes from form submission to first live contact, with under 60 seconds as the target. Mortgage borrowers shop several lenders in one sitting, so the lender who reaches them first usually controls the conversation. Research on lead response found the odds of qualifying a lead fall sharply, roughly 21x, when callback time slips from 5 minutes to 30, and they keep dropping minute by minute after that. Measuring to assigned or emailed does not count; the clock that matters runs to the first live human touch.

Why does mortgage lead response time matter so much?

Because a rate-shopping borrower rarely fills out one form; they submit three or four lender forms at roughly the same minute. At the moment of contact they have not compared rates yet, they are comparing who picked up. The first lender to reach them gets to set expectations and start the application while everyone else waits in a queue. That first-mover advantage is why minutes, not hours, decide which lender wins the loan.

How fast can Aloware call a mortgage lead after a form submission?

Aloware's Form2Call routes a new lead to an available loan officer within about 60 seconds of the form submission, with the borrower's details previewed before the call connects. In parallel, Form2Text sends the borrower a personalized SMS within seconds, so they know a loan officer is calling. The combination means the borrower hears from you across two channels inside the first minute, instead of waiting for someone to work a queue.

Is texting a mortgage lead first a TCPA problem?

A borrower who submits your lead form has typically given express consent to be contacted, which is what makes an instant text and callback appropriate, but that depends entirely on how your form, disclosures, and consent capture are configured. Aloware sends from registered A2P 10DLC numbers, which supports deliverability and good standing. Treat the consent and disclosure setup as something to configure deliberately with whoever owns compliance at your company, not something to improvise.

What happens to mortgage leads that come in after hours?

This is where many teams quietly lose leads. With Aloware, after-hours form leads queue to the top of the next morning's call list so they are the first thing a loan officer works. For inbound calls that arrive when no one can pick up, AI Call Rescue answers automatically, greets the caller, captures their intent and contact details, and logs the conversation, so a 9 p.m. lead does not sit untouched until someone notices it.

Does speed-to-lead automation replace my loan officers?

No. The instant text and missed-call recovery buy time and hold the borrower's attention so they do not drift to a competitor while your team is busy. The loan officer still qualifies and closes. The automation handles the part humans cannot win, being instant every time including nights and weekends, and hands a warm, logged lead to the LO. Teams that frame it as the system selling for us set the wrong expectation.

How does Aloware log mortgage lead activity in my CRM?

Every touch, the instant text, the callback, a recovered missed call, the AI voice agent transcript, writes back to the borrower's contact record automatically, in real time. Aloware maps to actual CRM entities rather than dropping a generic activity log, so a loan officer opening the record sees the full timeline and works from context instead of reconstructing what happened. That removes the manual logging that usually eats an LO's day.

What's the difference between Form2Call and Form2Text?

Form2Text sends a personalized SMS to the borrower the instant a form is submitted, fast acknowledgment that holds your place while a loan officer dials. Form2Call routes that same lead to an available loan officer's phone within about a minute, with the borrower's details on screen for a warm first call. They are designed to run together: the text reaches the borrower in seconds, the call follows right behind, and the borrower hears from you on two channels before competitors get to one.

.png)

Brandi Rice is the VP of Revenue at Aloware, focused on the operational side of running a contact center: SDR onboarding, connection-rate diagnostics, A2P 10DLC and STIR/SHAKEN compliance, healthy calling behavior, and the KPIs that predict revenue. She writes for sales managers, RevOps leaders, and ops practitioners.

--How-Fast-Sales-Teams-Actually-Respond.webp)